Notes from the desk

The Broken Slot Machine: Why Alpha Erodes, and What Stays

Alpha is real, but it erodes. Every edge ever found has been slowly arbitraged away by the market — a self-equilibrating machine that fixes its own glitches. Yet some things persist.

Imagine a casino floor full of slot machines. Most are standard. But one has a glitch — pull the lever and it pays out slightly more often than it should. You find it. You play it. You make money.

But here's the thing: every quarter you feed into that machine is data. Someone watches the payout pattern. Writes a paper about it. Traders read the paper. More capital flows in. And slowly, the “glitch“ gets repaired. The machine returns to normal. The edge is gone.

Then you wander the floor looking for the next broken machine.

That's alpha. And this is why it never stays.

What we used to call alpha

In the old framework, alpha was simple: if the market returned 10% and your portfolio returned 14% with the same risk, those extra 4 points were your skill. You saw something others didn't. You had an edge. The industry charged 2-and-20 for it. A generation of fund managers built careers on it.

Then in the early 1990s, Eugene Fama and Kenneth French looked under the hood and found that most of what was called "skill" was really just exposure to risk factors — small companies, cheap stocks — that anyone could replicate for a fraction of the fee. More factors followed: momentum, profitability, low volatility, quality. Every time researchers found a new one, the chunk of return that could honestly be called "alpha" got smaller.

The self-fixing market

There's a famous paradox by economists Grossman and Stiglitz that explains why this happens. Think about it: if markets were perfectly efficient — if every piece of information was already priced in — there would be no reason to do research, because you couldn't profit from being smarter. But if nobody does research, prices stop reflecting information. So the market settles somewhere in the middle: enough people gather information to keep prices roughly right, but not so right that there's no reward for being the first to spot something.

This is the self-fixing mechanism. Every mispricing is an invitation. The first person through the door gets paid. But the act of exploiting it — buying what's cheap, selling what's expensive — pushes prices back where they belong. The more capital that piles in, the faster the edge compresses. The market fixes itself, the same way a broken slot machine eventually gets repaired by the floor manager.

There are limits to how fast this happens — short-selling restrictions, transaction costs, the risk that the mispricing widens before it collapses. These frictions slow the process, but they don't stop it. The academic consensus is clear: competitive arbitrage eventually neutralizes persistent, risk-adjusted alpha.

Four edges that were once gold

Trend following

Buy when price is above its 200-day moving average. Move to cash when below. For decades, this simple rule delivered 6–10% annual abnormal returns. Sharpe ratios near 1.2. It was free money — or close to it.

By the 2010s, the same strategy was delivering 1–3%. AQR's professional trend-following programs fell from 12%+ annual returns in the early 2000s to high single digits. The strategy didn't break. It just got crowded. More traders chasing the same trends meant trends became shallower. The edge didn't disappear — it compressed.

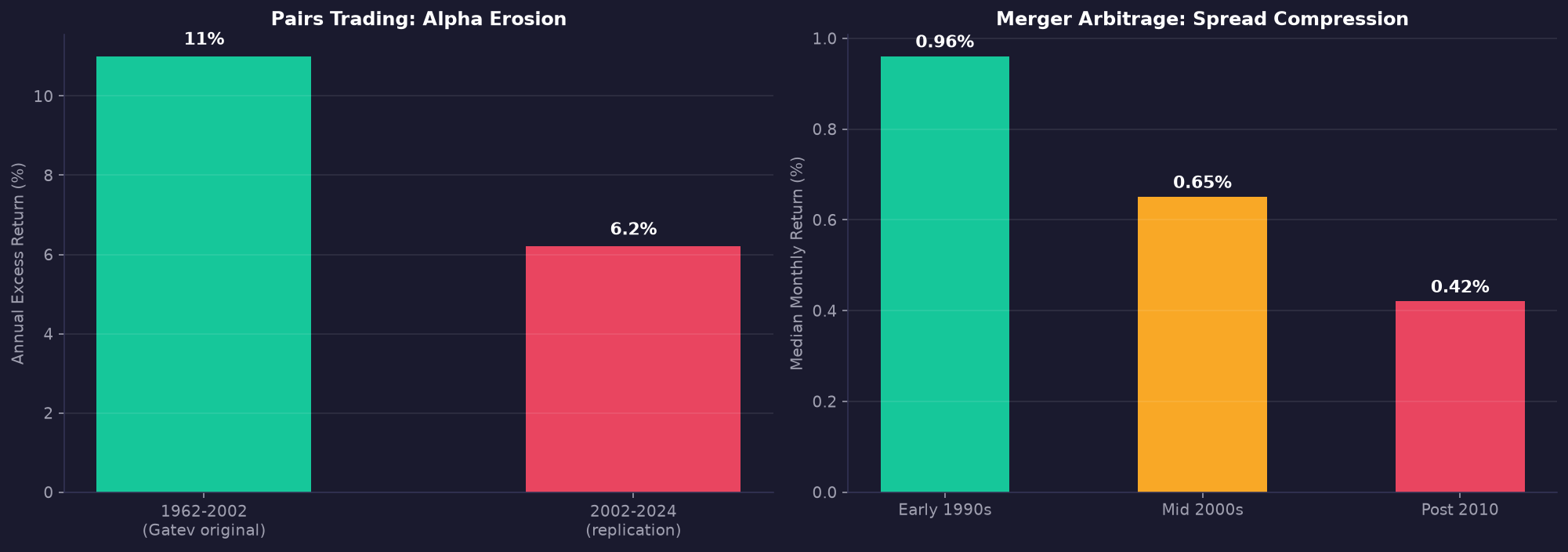

Pairs trading

In the 1970s, a group at Morgan Stanley started a simple trade: find two stocks that move together, bet on the spread between them reverting. It worked brilliantly. In the 1990s, firms like Renaissance Technologies and D.E. Shaw built hedge fund empires on this idea. Academic studies documented 11% annual excess returns.

A 2024 study found the same strategy today delivers about 6.2%. Still positive, but nearly cut in half. The mispricings that powered the original gains got arbitraged away — exactly as the theory predicts. Sub-period analyses show profits declining in every successive five-year window.

Merger arbitrage

Buy the target company, short the acquirer, collect the spread between the two prices. In the early 1990s, this paid roughly 0.96% per month. By the mid-2000s: 0.65%. Post-2010: below 0.5%.

The spread compressed because more people piled in. Lower trading costs, more analyst coverage, dedicated hedge funds — all pushing the premium toward zero. The strategy still works. It just pays half what it used to, with more capital deployed to capture less.

Convertible bond arbitrage

In the 1990s and early 2000s, convertible arbitrage generated roughly 13% annual returns with almost no volatility — a Sharpe ratio that most retail strategies would envy. By the 2010s, after a decade of flat performance, the edge was gone. Too many hedge funds crowded the same trades, driving the mispricing too thin to profit from. The approach became, in one analyst's words, "a meagre source of returns."

How much alpha was ever real?

There's a well-known study by Harvey, Liu, and Zhu that looked at roughly 300 different stock-picking strategies that academics had published. They found that most of them wouldn't survive a basic statistical sanity check. With 300 researchers testing 300 different ideas, some are going to look significant just by chance. The majority of published factors, they concluded, were probably false discoveries — data-mining dressed up as insight.

The practical evidence backs this up. Year after year, the SPIVA scorecards show that roughly 80% of actively managed US stock funds underperform their benchmark over a decade. The performance gap widens with time. Most managers can't sustain positive alpha over the long run. Not because they're bad — because the market is a self-fixing machine.

The broken slot machine

Here's where all of this comes together.

The market is a casino full of slot machines, and most of them have a glitch somewhere. The first person to find a glitch makes money. But every quarter you put in is data. Someone watches. Someone writes a paper. Capital flows in. The “glitch“ gets repaired across time.

What stays

The thing that doesn't erode is not a mispricing at all. It's a risk premium.

The equity risk premium — the extra return stocks earn over risk-free bonds — has persisted across centuries. Estimates tracing it back to the 1800s find an average of about 7%. It survives because it's not an inefficiency. It's compensation for holding something that can drop by 50% and take a decade to recover. As long as stocks are risky and most people prefer safety, that premium exists.

Competition can erode a mispricing. It can't erode the compensation for bearing systematic risk. The discomfort is structural. You can't arbitrage away the fact that volatile assets need to pay more to attract capital.

Smart beta — buying a basket of value stocks, or momentum stocks, or low-volatility stocks — sits in this middle ground. The factor has been discovered, documented, and commoditized. But the underlying premium survives because it's rooted in risk, not in a glitch. Value stocks earn more because they're more painful to hold. Momentum stocks earn more because buying what's already run up is uncomfortable. Both discomforts persist because they're human. Competition can't fix that.

The broken slot machine will keep paying out — just often enough to keep the dream alive. Alpha is real, and people will keep chasing it, and some will even find it. But the only edge that stays is the one that doesn't need to be found in the first place: harvesting the premium that exists because someone has to hold the risk, and that someone gets paid.

Educational, not financial advice. This article draws on academic research including Grossman-Stiglitz (1980), Fama-French (1993), Gatev et al. (2006), Harvey, Liu & Zhu (2016), and the SPIVA scorecard series. Past performance does not guarantee future results.